Discover what ION can do for you

Ultra-low latency FX trading solutions

Barracuda FX is a global leader in end-to-end, modular, customizable eFX trading solutions for financial institutions operating in foreign exchange markets.

The Barracuda FX connectivity and trading solutions provide low latency access to all major OTC markets and bank liquidity providers. Prices are aggregated to provide normalized views of sweepable, full amount, and RFS liquidity distributed to the trader user interface and APIs. Orders are intelligently worked by the smart order router to minimize slippage and market impact.

Advanced eFX pricing, hedging and order management

eFX pricing and distribution modules allow you to seamlessly integrate in-house proprietary logic with Barracuda FX pricing smarts.

An extensive range of intelligent pricing options give you the flexibility to create differentiated, competitive spot and forward pricing tailored to the needs of your clients, distributed across all internal and external channels, auto risk managed.

The Barracuda FX OMS won the P&L Reader’s Choice Awards for Best FX OMS for 10 conseutive years. It is deployed as the global order book in over 20 of the top 50 banks globally and supports resting, fixing, and algorithmic orders in FX and precious metals with native access to Order Hub.

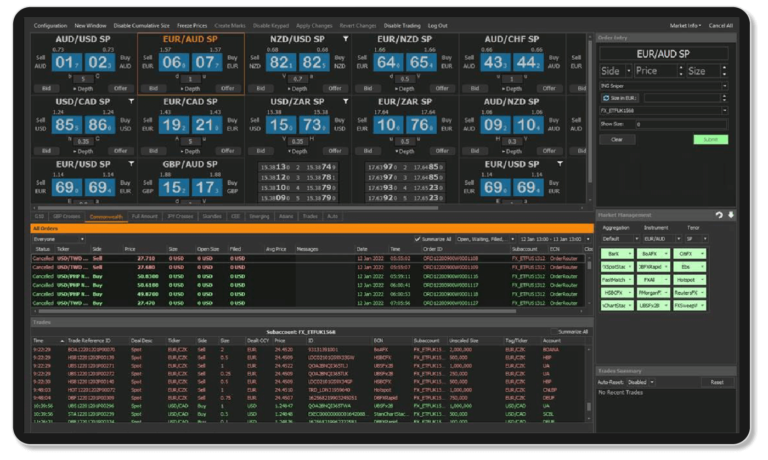

Connectivity and trading

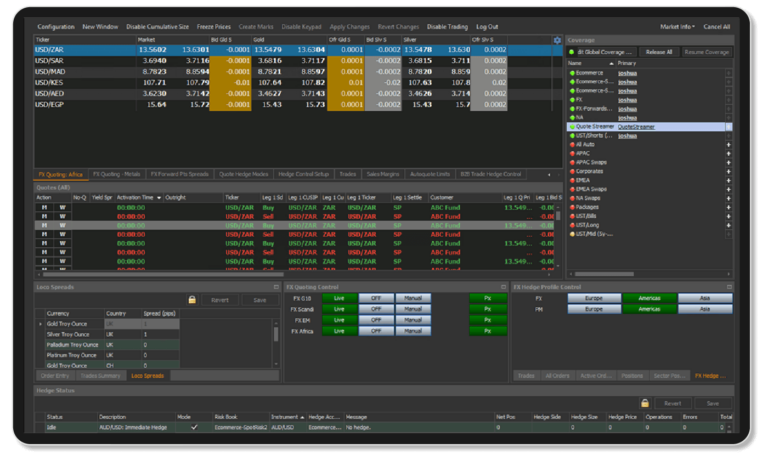

Pricing, distribution and risk

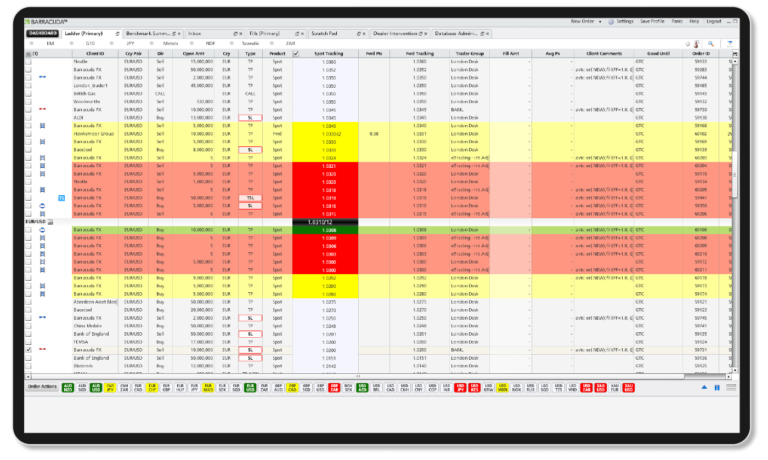

Order management system

Ultra-low latency

High performance

Modular technology

Key features

Connectivity and trading

Ultra-low latency connectivity to OTC markets.

Fully customizable liquidity aggregation.

Powerful dynamic smart order routing and execution algos.

Normalized API for integrating custom execution strategies.

Sophisticated crossing engine to create synthetic tradeable markets.

Real-time analytics and performance benchmarking.

Pricing, distribution, and risk

Componentized intelligent pricing engines for metals, G10, EM, and frontier markets, enabling IP injection throughout the pricing pipeline.

ESP, RFQ, and RFS price negotiation for spot, forward, swap, NDF, NDS, blocks, money markets, and all post-trade actions.

Deterministic low-latency price distribution across all internal and external distribution channels including all major multi-dealer portals.

Real-time position management and a rich suite of advanced rules driving hedging strategies to maximize internalization opportunities.

High-performance dealer and sales desktops for quote negotiation and on-behalf of dealing.

Order management system

Automated management of resting, fixing and algorithmic orders in spot, forward, NDF and precious metals.

Tightly integrated to the bank’s auto-risk management environment and natively connected to Order Hub

Distribution gateways to all major multi dealer portals, bank’s single dealer platforms and FIX API.

Latest Markets awards

GW Platt FX Tech Awards 2023

FX Markets e-FX Awards 2022

TradingTech Insight USA Awards 2022

GW Platt FX Tech Awards 2022

Related products

Wallstreet FX

High-performance, real-time trade processing solutions for currency management.

Spectrum

A complete foreign exchange solution for brokers and wealth managers, providers of international payments and FX hedging services, and treasury teams.

FX Operations

Process all forex transactions, confirmations, settlements, and payments worldwide on one platform.

FX Trade and Risk Management

Do all your forex trade processing and risk management across instruments and get a complete, real-time view of your business.